-

Know where you stand

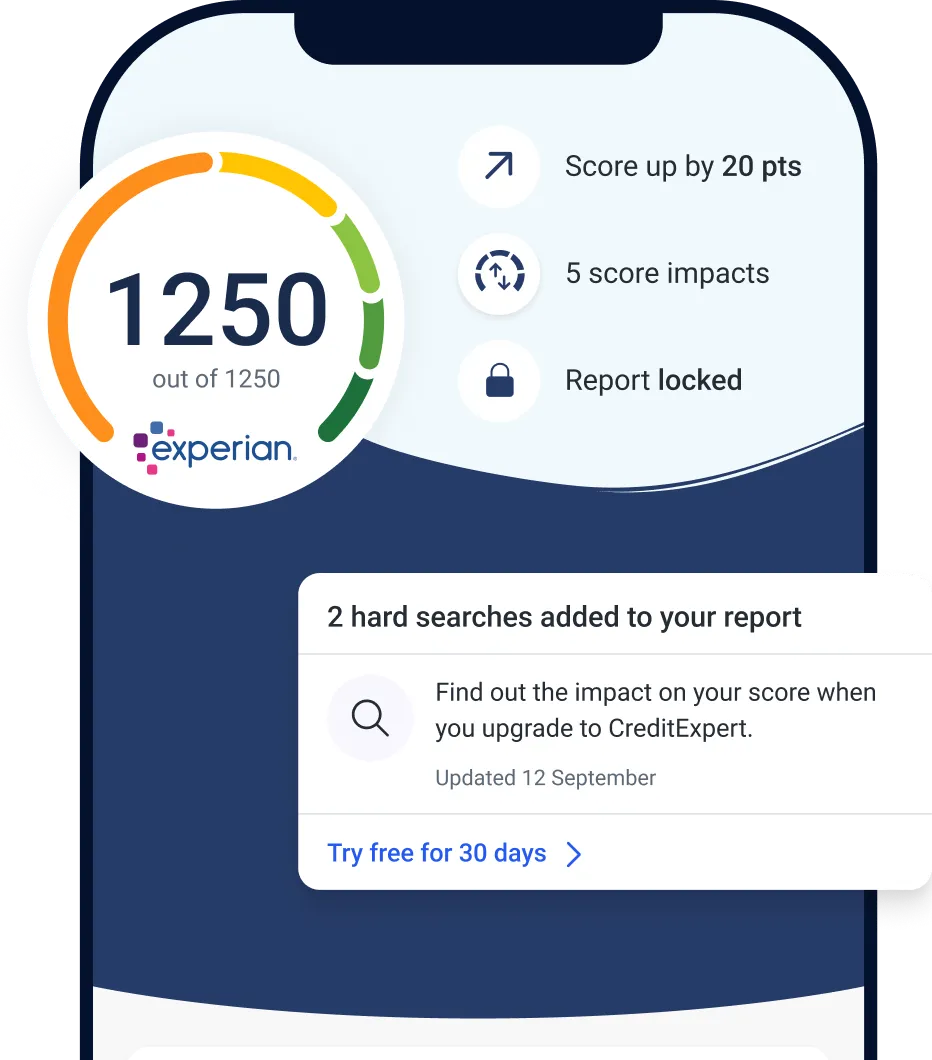

Your credit score shows how lenders view you

-

Control of your finances

Get a breakdown of your borrowing in one place

-

Credit with confidence

Check your chances of getting credit cards and more

Why is your score important?

The higher your score, the better your chances of being accepted for things like credit cards, mortgages, loans and more.

How is your credit score calculated?

Your Experian Credit Score is based on information in your Experian Credit Report, such as:

- Your payment history – do you always pay accounts on time, or do you have late payments or defaults?

- How much you owe – if you're always close to your credit limit, lenders may think you're in financial difficulty

- How often you apply for credit – too many applications in a short space of time can harm your score

Find out more about what affects your score.

Get my free score

What's a good credit score?

Your Experian rating explained

Whether you want to get a house, car, loan or credit card – getting the UK's leading credit score could help you meet your money goals.

Get my free scoreExcellent

1121 to 1250

You should get the best credit cards, loans and mortgages (but there are no guarantees).

Very Good

1001 to 1120

You should get most credit cards, loans and mortgages – but you might not get the very best deals.

Good

861 to 1000

You should see a wide range of credit cards, loans and mortgages – but you might have to pay a bit more interest.

Fair

641 to 860

You might get limited credit options, higher interest rates, and lower borrowing limits. But our tools can help improve your score. And as it grows, so will your choices.

Low

0 to 640

Borrowing may be difficult and interest rates could be high. But our tools can help get your score moving in the right direction. Every small increase helps, and things should improve as you get closer to a Fair score.

Frequently asked questions

The average Experian Credit Score is 850. But if you score below this, don't worry. You may still qualify for plenty of deals.

Plus we've got lots of tips on how to improve your credit score.

Once you've got your free Experian Credit Score, see if you can instantly improve it using Experian Boost.

Normally, payments for things like council tax, savings accounts, and subscriptions (such as Spotify and Netflix) don't count towards your score. With Experian Boost, they do.

Not all credit scores will increase with Boost – but using it will never make your score go down. Find out more about Boost.

It's a good idea to regularly check your score, especially if you're planning on applying for credit in the future.

Check your score as often as you like, it won't harm it!

Absolutely! We work with the UK's leading lenders to give you deals you won't find anywhere else. What's more, we can help match you to offers based on your credit score – so you can apply with confidence. We do all the legwork so you don't have to.