Monthly Sector Insights

Welcome to Experian’s Monthly Sector Insights blog

Your go-to resource for the latest trends and analysis of consumer spending across key sectors. Our insights are derived from our Consumer Dynamics Spend Insights data, which is updated monthly.

We analyse over 180 million transactions and £8 billion in monthly spend to generate a comprehensive view of consumer behaviour. The data encompasses various sectors, including retail, leisure, and travel & transport and enables us to understand where spending is occurring, the types of demographic groups making the spending, and by which channel (online vs offline).

Jump to sector: Retail | Leisure | Travel & transport

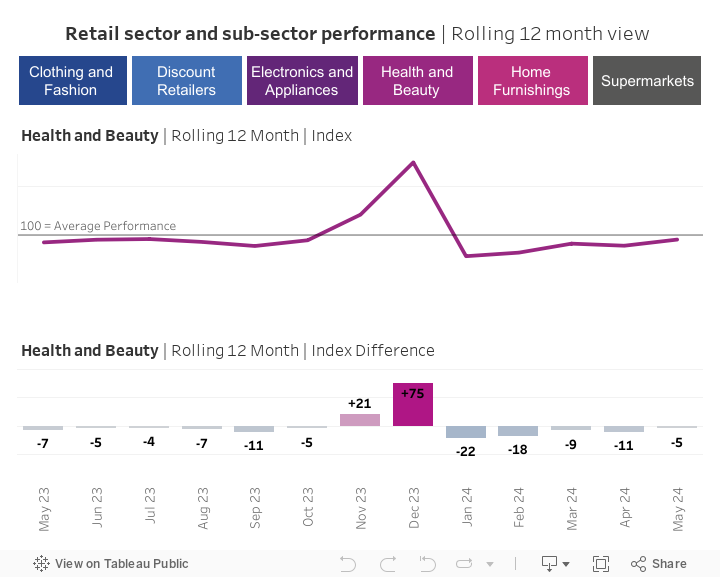

Sector: Retail

The chart above enables you to view spend across the relevant sub-sectors for the last 13 months. The performance of each month is displayed as an index compared to the average performance across the previous 12 months (August 23 – July 24). An index of 100 indicates that performance across a given month is the same as the average spend. An index of 120 indicates spend 20% above average and an index of 80, 20% below average.

According to Experian’s Spend Insights panel data, consumer spending across the UK retail sector in July 2024 remained largely consistent with both June’s figures and the same period in 2023.

The clothing and fashion sector experienced a slight decline, with sales down 0.4% compared to July 2023 and 1.4% from the previous month as warmer weather failed to fully convince consumers to transition to summer wardrobes.

We have previously noted the ongoing challenges in the Home Furnishings and Electronics & Appliances sectors, driven by the rising cost of consumer credit and a sluggish housing market and this trend persisted in July. While the Electronics & Appliances sector saw a slight rebound from June, overall spending remained significantly lower than in July 2023 across both sectors.

Looking ahead, the UK retail sector continues to face significant challenges in the second half of the year. Despite some positive economic signals, government efforts to address the national spending imbalance may further impact consumer spending.

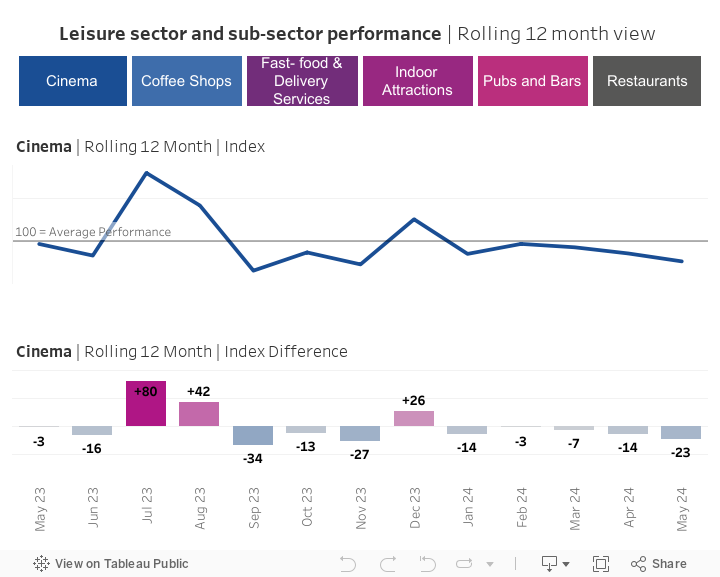

Sector: Leisure

The chart above enables you to view spend across the relevant sub-sectors for the last 13 months. The performance of each month is displayed as an index compared to the average performance across the previous 12 months (August 23 – July 24). An index of 100 indicates that performance across a given month is the same as the average spend. An index of 120 indicates spend 20% above average and an index of 80, 20% below average.

As the school holidays commenced at the end of July, consumer spending saw a modest increase compared to June’s figures. However, overall spending across the leisure sector was down approximately 6% compared to the same period last year. Improved weather conditions towards the latter part of the month, coinciding with the start of the summer break meant consumers where able to spend time outdoors with a reduced need for indoor activities.

However, the cinema sector did experience a notable uptick, driven by strong visitor numbers to new releases – *Despicable Me 4* and *Deadpool and Wolverine*. This increase helped offset the slow start to 2024, although the observed spend was still some way below the “Barbenheimer” phenomenon of July last year.

Meanwhile, Restaurants, Pubs, and Bars continued to face significant challenges in attracting consumer spending, with both sectors reporting a notable decline compared to the same period in 2023—despite the improved weather and the excitement of England reaching the Euro 2024 finals.

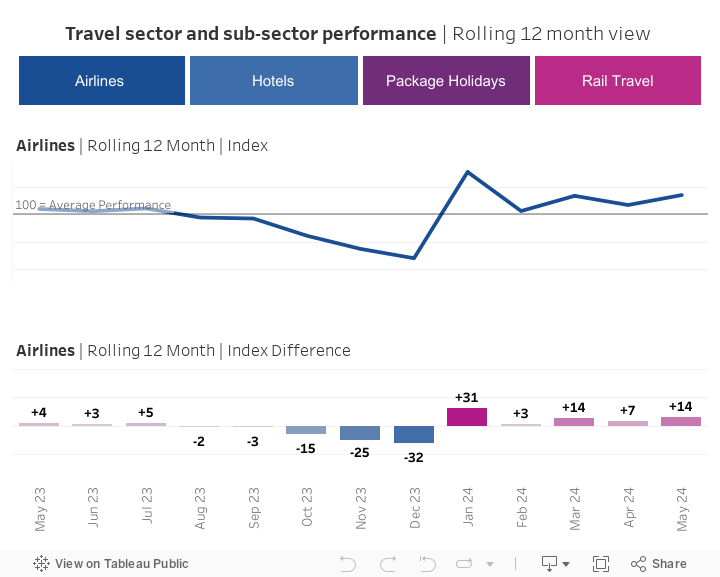

Sector: Travel & transport

The chart above enables you to view spend across the relevant sub-sectors for the last 13 months. The performance of each month is displayed as an index compared to the average performance across the previous 12 months (August 23 – July 24). An index of 100 indicates that performance across a given month is the same as the average spend. An index of 120 indicates spend 20% above average and an index of 80, 20% below average.

Demand for outbound travel from the UK continued its strong upward trajectory in July, according to our Spend Insight panel data. Total sector spending increased by 9.2% compared to July 2023, highlighting the UK consumer’s ongoing preference for holidays and travel over other discretionary spending categories.

Spending on airlines rose by 2.2% compared to June and saw an impressive 8% increase year-on-year. Although spending on package holidays experienced a slight dip from June levels, it surged by 12% compared to July 2023, demonstrating the continued appeal of pre-planned vacations for UK travelers.

Domestic travel also saw a significant boost. Spending on UK-based hotels, which had been sluggish in previous months, experienced a marked uptick in July. This coincided with the start of the school holidays and improved weather, which also contributed to a rise in rail travel.

Overall, the travel sector remains a standout in the UK’s consumer spending landscape, with both international and domestic travel benefiting from strong demand, as families and individuals prioritise leisure and experiences during the summer months.

Join our Marketing Insights Forum

If you’re not already a Marketing Insights Forum member, register today for regular trends reports on consumer behaviour and attitudes specific to your sector. Members also have access to a sector-specific consultant who will provide insights and solutions to help you overcome your business challenges.

For any questions or to learn more about our services, please contact us at:

Further reading

Marketing insights webinar – The future of UK travel and leisure

Watch our webinar where we leverage Experian’s Consumer Dynamics Insight to dissect the latest market developments and behavioural trends.

Marketing insights webinar – Unwrapping consumers’ Christmas behaviours

Watch this webinar now and equip yourself with invaluable insights that transform your approach to holiday marketing!

Ask the Expert: Audience insights for advertising agencies with IPA

In this episode we discuss the role of audience insights in a cookieless future, exploring how agencies can effectively understand and target audiences.

Ask the Expert: Mobility data with Visitor Insights

In our ongoing ‘Ask the Expert’ Q&A series, we guide you through a discussion on how mobility data can drive better business and marketing strategies.

Google’s cookie turnaround

In this blog we discuss the decision for Google to reverse its plan to deprecate the third-party cookies in Chrome and what it also means for businesses.

Ask the Expert: Sell-side targeting in digital media with PubMatic

This episode delves into programmatic digital media, revealing how PubMatic plays a pivotal role in enabling content creators to monetise their assets.

Ask the Expert: Addressable TV advertising with Finecast (part two)

In part two of this insightful ‘Ask the Expert’ Q&A series, we delve into the complexities of defining audiences in data-driven TV advertising.

Focussing cost of living support through data driven insights with Lambeth Council

Experian works with Lambeth Council to deliver a data-driven solution to better understand the impact of the cost of living crisis on its residents.

Experian helps Interflora make every delivery special

Learn how our Address Validation helps Interflora reach thousands of consumers and supports operations from the order process through to door-step delivery.

The cost-of-living crisis – predictions for 2023

As we leave 2022 and enter the New Year the UK is still deep in a Cost of Living crisis but what is the forecast for 2023 and beyond? Find out more.