Understand the impact BNPL spend has on an individual’s credit worthiness

In July 2022, we released our first guide for lenders on insight revealed from our analysis of Buy Now, Pay Later (BNPL) transactional data being shared into our bureau.

With more data from multiple lenders now flowing into our bureau, this second paper seeks to build on this original analysis to assess the impact of BNPL against the backdrop of increases in the cost-of-living, squeeze on household incomes and forthcoming Christmas shopping season.

Get to the heart of how consumers are using BNPL services to manage their finances, and what this means for lenders.

Uncover our latest research

Lenders need to start considering the role of BNPL transaction data in understanding the full extent of an individual’s credit commitments, to better understand and monitor financial well-being, ensure good outcomes and to demonstrate adherence to Consumer Duty.

Use of BNPL continues to grow

As of September 30th 2023, Experian had processed a total of 53.8m BNPL transactions with a combined value of £3.7bn across 5.9m unique customers.

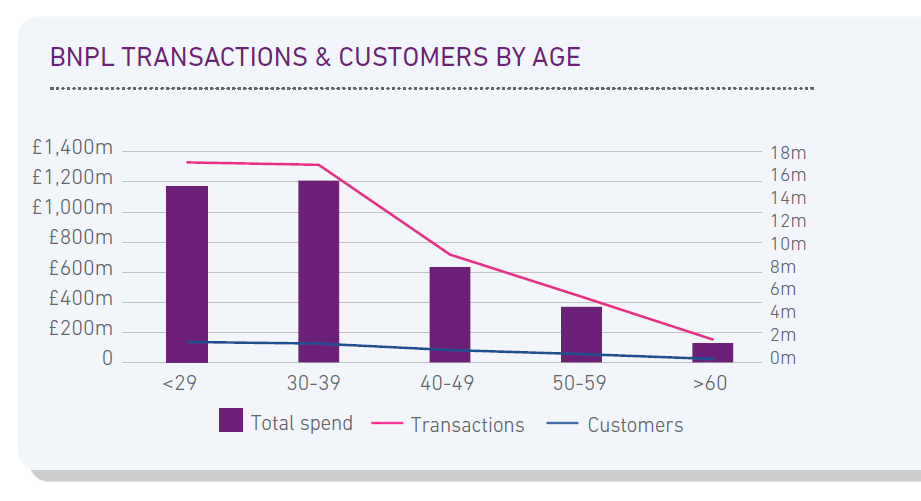

The largest user base comes from those aged 39 or younger who represent 57% of all users

But throughout 2023 the fastest growth came from older, less risky customers aged between 45-64.

The number of customers making at least one transaction a month remains consistent at 2m

The average number of transactions made by each customer decreases with age. However, for all age bands we see the highest transaction value is over £2,300.

In this report, we cover:

Transaction volumes

Our analysis suggests that the volume of BNPL transactions in the UK will continue to grow

Behaviour and spending trends

BNPL is still widely favoured by younger consumers who have very different attitude towards credit

Credit consumption

With BNPL providers now sharing consumer’s transaction data with credit bureaux, Experian can provide lenders with a more complete view of a customer’s credit consumption that includes visibility on their use of BNPL

Getting a more accurate understanding of risk

Given the transactional nature of BNPL, and the short outcome period, Experian has been able to develop a view on the performance of BNPL services and how this compares to other products

A sneak peek into:

Getting the full picture: Making Buy Now, Pay Later payments visible

Behaviour and spending trends

By some distance the largest user base comes from those 39 or younger and these customers represent 57% of all users. This is split equally between those 18-29 (29%) and 30-39 (28%) with the numbers then decreasing as we progress through the age bands.

Over the 10-month period, we see the average number of transactions made by each customer decrease with age: the figure peaks at 10 transactions with an average spend of ~£740 in the 30-39 age band dropping to 6.2 at an average spend of ~£400 for those 60 or over.

These, however, are only averages and for all age bands we see the highest transaction value being in excess of £2,300. This is why lenders need to look at each consumer individually when assessing their use of BNPL versus their consumption of other sources of credit.

Did you enjoy the read?

Download the report "Getting the full picture: Making Buy Now, Pay Later payments visible"

Read our paper to get to the heart of how consumers are using BNPL services to manage their finances, and what this means for lenders.

Further reading

Five things BNPL lenders should consider when measuring consumer credit worthiness

In 2020 use of Buy Now, Pay Later credit almost quadrupled in the UK. What should lenders consider as they prepare for possible regulation?

Responsible BNPL regulations: Lenders can get ahead of the game now

This article explores how BNPL providers should engage with bureaux.

Buy Now, Pay Later myth-busting: Who’s using it, how much are they spending, and how risky are they?

We debunk eight assumptions about BNPL, and take a deeper look into who uses BNPL services and how consumers are engaging.

4 ways to reduce your identity fraud losses

Identity fraud continues to be a significant threat. Find out how to effectively reduce your ID fraud losses with these essential strategies.

What you need to know about Money Mules

Money muling isn’t a new phenomenon, but social media has made it easier than ever for criminals to find willing mules.

Vital income and employment verification documents

Learn about different income and employment verification documents to meet employees’ needs and provide support they need during big-life moments.

Why good quality data will be essential for Gen-AI

Accurate data ensures reliable AI outcomes, while a single customer view consolidates information to better understand behaviours and preferences.

What is the key to agile lending in a competitive market?

Over 65% of UK organisations report that it’s still taking too long to develop and deploy new credit decisioning models. What is the answer?

The Commercial Delphi Score explained

Find out all you need to know about the Commercial Delphi score - a rating system for business creditworthiness.

Three methodologies for assessing commercial affordability

Assessing commercial affordability can be a complex task. In this blog, we will discuss three key ways to assess commercial affordability.